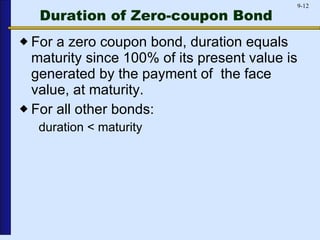

42 zero coupon bonds duration

Zero-coupon bond - Wikipedia Zero coupon bonds have a duration equal to the bond's time to maturity, which makes them sensitive to any changes in the interest rates. Investment banks or dealers may separate coupons from the principal of coupon bonds, which is known as the residue, so that different investors may receive the principal and each of the coupon payments. That creates a supply of new zero … Duration Definition and Its Use in Fixed Income Investing - Investopedia 01/09/2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

Join LiveJournal Password requirements: 6 to 30 characters long; ASCII characters only (characters found on a standard US keyboard); must contain at least 4 different symbols;

Zero coupon bonds duration

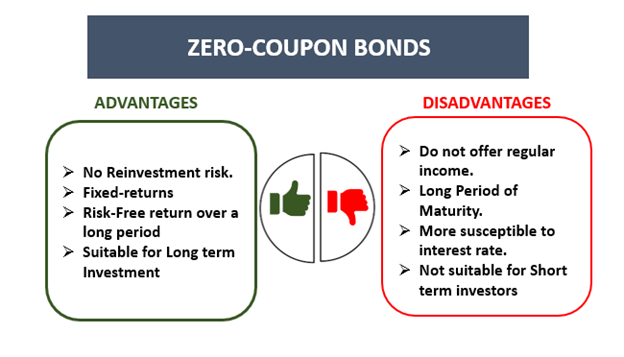

Zero Coupon Bond Value Calculator: Calculate Price, Yield to ... If rates fall longer duration zero-coupon bonds will increase in value significantly more than shorter duration federal government bonds & federal bonds which pay a regular coupon. If rates rise the converse is true - zero-coupon bonds will be hit much harder than other bonds. Negative Yields . After the financial crisis of 2008-2009 central banks became far more aggressive … How to Calculate Yield to Maturity of a Zero-Coupon Bond 10/10/2022 · Corporate zero-coupon bonds are usually riskier than similar coupon-paying bonds. If the issuer defaults on a zero-coupon bond, the investor has not even received coupon payments, so the potential ... Zero Coupon Bond Calculator – What is the Market Price? - DQYDJ Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) Zero coupon bonds are particularly sensitive to interest rates, so they are also sensitive to inflation risks. Inflation both erodes the ...

Zero coupon bonds duration. Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia Jan 31, 2022 · Zero-coupon bonds are also appealing for investors who wish to pass wealth on to their heirs but are concerned about income taxes or gift taxes. If a zero-coupon bond is purchased for $1,000 and ... The One-Minute Guide to Zero Coupon Bonds | FINRA.org Oct 20, 2022 · Like virtually all bonds, zero coupon bonds are subject to interest-rate risk if you sell before maturity. If interest rates rise, the value of your zero coupon bond on the secondary market will likely fall. Long-term zeros can be particularly sensitive to changes in interest rates, exposing them to what is known as duration risk. Also, zeros ... Bonds & Rates - WSJ Stocks: Real-time U.S. stock quotes reflect trades reported through Nasdaq only; comprehensive quotes and volume reflect trading in all markets and are delayed at least 15 minutes. Understanding Bond Prices and Yields - Investopedia Jun 28, 2007 · Bond Prices and Yields: An Overview . If you buy a bond at issuance, the bond price is the face value of the bond, and the yield will match the coupon rate of the bond.

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. Zero Coupon Bond Calculator – What is the Market Price? - DQYDJ Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) Zero coupon bonds are particularly sensitive to interest rates, so they are also sensitive to inflation risks. Inflation both erodes the ... How to Calculate Yield to Maturity of a Zero-Coupon Bond 10/10/2022 · Corporate zero-coupon bonds are usually riskier than similar coupon-paying bonds. If the issuer defaults on a zero-coupon bond, the investor has not even received coupon payments, so the potential ... Zero Coupon Bond Value Calculator: Calculate Price, Yield to ... If rates fall longer duration zero-coupon bonds will increase in value significantly more than shorter duration federal government bonds & federal bonds which pay a regular coupon. If rates rise the converse is true - zero-coupon bonds will be hit much harder than other bonds. Negative Yields . After the financial crisis of 2008-2009 central banks became far more aggressive …

Duration | Definition & Examples | InvestingAnswers

Price of a defaultable zero coupon bond price in each time t ...

Floating Rate Notes Pricing and Valuation | FinPricing

Understanding Fixed-Income Risk and Return | IFT World

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

Modified Duration - Zero Coupon Bond Modified Duration ...

Modified duration of zero-coupond bond (FRM practice question)

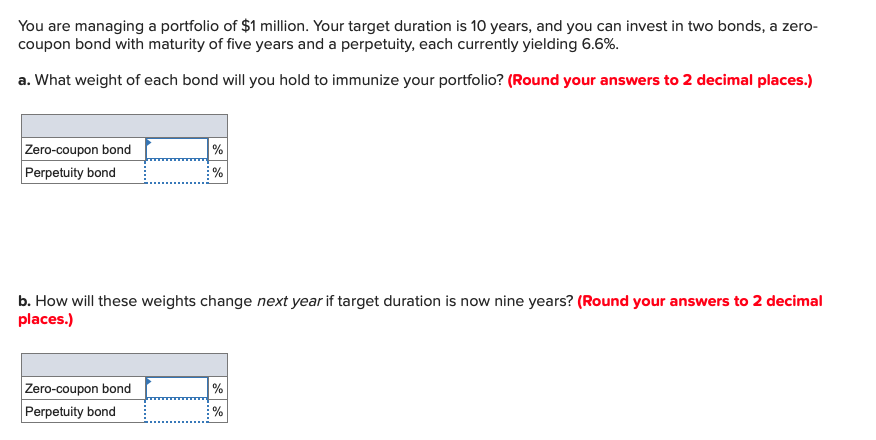

Solved You are managing a portfolio of $1 million. Your ...

Duration: a measure of bond price volatility | Nuveen

Zero Coupon Bond - QS Study

PPT - Bond Price Volatility PowerPoint Presentation, free ...

Bond Economics: Primer: Par And Zero Coupon Yield Curves

Answered: Duration and Convexity (Part 2): A bond… | bartleby

What is the duration of a zero-coupon bond that has eight ...

Zero-coupon bond - PrepNuggets

Olympus Treasuries: Zero-Coupon Bonds for Flexible Staking ...

Investment Improvement: Adding Duration to the Toolbox | St ...

VALUING BONDS

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

The Cash Account and Pricing Zero-Coupon Bonds - Term ...

What is the duration of a zero-coupon bond that has eight ...

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

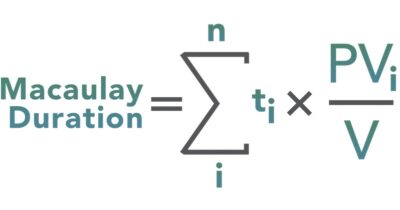

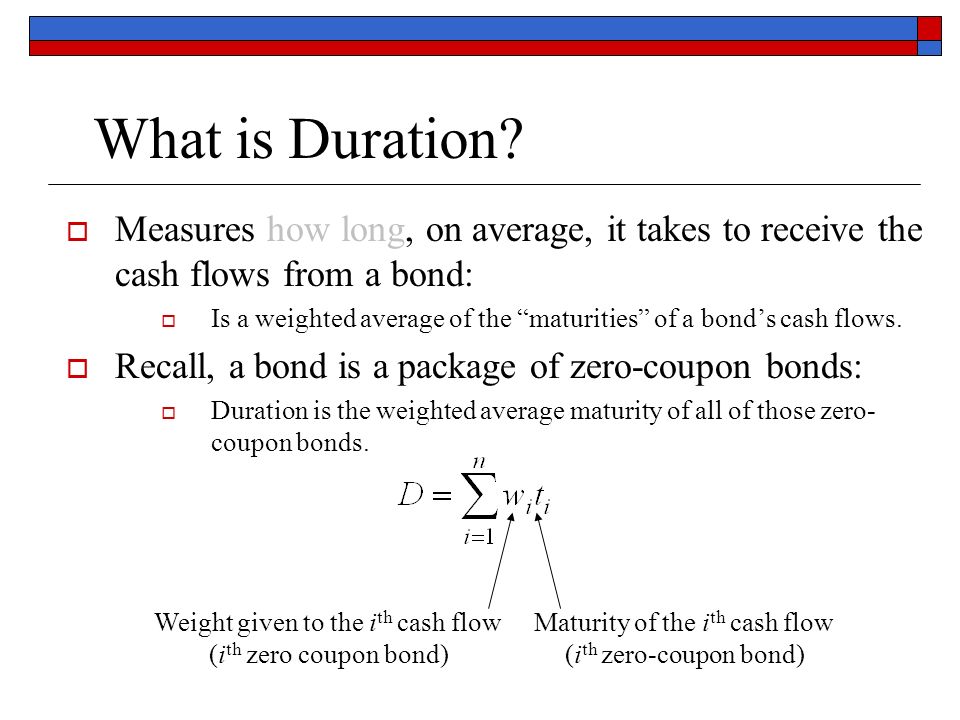

Macaulay Duration

A default-free zero-coupon bond costs $91 and will pay $100 ...

Solved] You are managing a portfolio of $3.0 million. Your ...

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

A 12.75-year maturity zero-coupon bond selling at a yield to ...

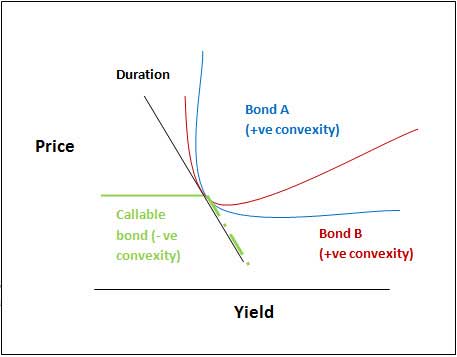

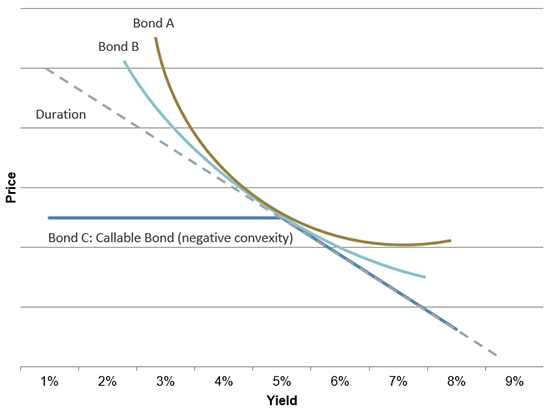

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bonds - Financial Edge

Interest Theory Final – Time: 70 min

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Under the Hood: What You Need to Know About Bond Duration and ...

Reserve Bank of India - Database

Duration & Convexity - Fixed Income Bond Basics | Raymond James

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Solved] 1) Assume you have a portfolio comprising 5 zero ...

Zero-Coupon Bond - an overview | ScienceDirect Topics

Portfolio Duration and its Limitations | CFA Level 1 ...

Duration model

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Post a Comment for "42 zero coupon bonds duration"